How to Calculate Your Net Worth and 3 Steps You Might Forget

Jan 08, 2021

What is your net worth, why is it important, and how do you calculate it?

Net worth is one of the most commonly tracked financial measurements. In this blog we're going to explore what your personal net worth is, why it's important and how you calculate it-- including some often forgotten steps!

What is your personal net worth?

Your personal net worth is simply the value that is left after subtracting your liabilities from your assets at a snapshot in time.

:max_bytes(150000):strip_icc():format(webp)/what-is-your-net-worth-be7a33afb9da4529abd5e376b5d325c2.png)

From thebalance.com

Why do you want to know your net worth?

- To create your goals: One of the best methods in financial planning is ‘reverse engineering.’ What do you want your personal net worth number to be? What do you need it to be to accomplish your life's goals? If you know this, then you can easily move backwards into your plan.

- To track your progress: Once you have a goal in mind, calculating your personal net worth on a regular basis can help you visualize your progress. This will keep you motivated to keep working at it. Sometimes we’re so busy doing the work, we don’t see the impact. I suggest calculating your personal net worth at minimum of 4 times a year, maybe more if you’re aggressively working a financial plan.

- To get an idea of your liquidity: Liquidity is just a fancy way to say — if you had to come up with X amount of cash, how easily could you do that? The concept of liquidity is important in emergencies or for accomplishing goals like buying a home or business — anything that requires a large lump sum of cash up front. Everyone’s level of liquidity is different.

- To use for lending purposes: Typically if you are applying for a mortgage or a business loan the lender will ask for some form of a personal net worth or ‘personal financial statement.’ If you have one ready, this could help speed up your lending process.

How do you calculate your net worth?

Here are my steps for calculating net worth:

- Tally up your assets- or what you own

- Tally Up your liabilities- or what you owe others

- What's the difference

- Know your credit score and factor that in

- Divide by your Adjusted Net Worth by your average monthly living expenses

- Remind yourself that your Net Worth does not equal Your Worth

- Repeat

Keep reading below to go through these steps one by one.

Want to make this process simple? My "Not a Budget" Cash Flow & Net Worth Workbook provides you with space to enter in your numbers and will auto-calculate your results. Plus- it's one workbook you can use ALL. YEAR. LONG. One download and your done!

Online tracker only? There are many to choose from. My current favorite is from Mint.

Step 1: Tally up your assets — or what you own.

There are two theories on what types of assets to include here. Some folks include ALL assets, others suggest to include income-producing assets only. The idea is that income-producing assets are what builds you wealth, anything else is really just…stuff. So if you’re uber focused on increasing cash-flow you might want to utilize this method.

Income producing assets include resources like rental property or stocks because they pay you money back. Your car, home, or TV are typically not paying you something back, so they go in the ‘stuff’ pile. It’s really up to you which method you prefer, I’ll add some of my thoughts under each category and you can decide on your own.

What you need to include in your assets:

- Cash in bank accounts

- 401K/ 403B Balances

- IRA Balances

- Investment account balances

- HSA balances

- Cash balances on life insurance policies or annuities

All this information should be pretty easy to find as it’s listed on your monthly statements. You can use today’s balance or take a look at your statement's most recent balance.

Here are a few things you may want to include that might be harder to quantify:

- Your primary residence

As I stated earlier, adding this to your assets pile is up to you. The idea is that your primary residence is not an income producing asset- because you are paying carrying costs (mortgage, taxes, insurance, maintenance) every month and it doesn’t pay you in return.

Some expectations might be if you run your business out of your home or if you utilize some or all of your property for rental space.

In addition, if your carrying costs are the same or less than what you would pay in rent, in my opinion I would include it.

Ways to look up real estate values: Using a licensed realtor or appraiser is the most accurate way to appraise a piece of property. You could also see if there has been a recent sale in your neighborhood and checkout the sale price/sqft. Using online real estate websites like Redfin, Zillow, Realtor, or Trulia can be used, but be aware that they are rarely accurate.

- Any other land or property

If you have rental property, you always want to include because if you have renters they are hopefully paying your carrying costs and maybe putting extra money in your pocket!

Use the same valuation strategy as your primary residence.

- Your personal vehicle

I rarely include cars in when calculating a net worth statement for myself or clients. Vehicles are a depreciating asset- meaning they lose value over time. In addition you also have a lot of carrying costs (gas, oil changes, insurance). Stay tuned for more content around why we think auto purchases are some of the biggest mistakes Americans make.

With all that said, here are the exceptions…

- If you have a classic car or a collectable vehicle

- If you rent out your vehicle

- You have had someone give you an offer for your car recently. Remember- a physical asset is only worth what you can sell it for.

- Personal items: This could include collectables, fine jewelry, or antiques.

Common examples of personal items you could include are a well taken care of instrument, a fine art piece, an antique piece of furniture, a designer handbag or diamond jewelry. Assets in this category can be appraised. The key is the item needs to be able to hold its value. So, my new iPhone definitely does not count!

Makes you take a second thought about your spending, right?!

- Holdings in any businesses

This could include a percentage of a partnership, LLC, or a corporation.

You’ll need to find the value (You can take the bank account balance + assets owned - debt for a quick estimate) of the business and calculate your percent.

- Receivable income

If you’ve lent money to friends or family you could include the balance that they owe you. However, friends and family don’t pay you back quickly if ever & lenders don’t always view this as an asset.

Step 2: Tally Up your liabilities- or what you owe others.

What you’ll need to include in your liabilities:

- Mortgage balances for both personal, secondary, and investment property

- Student loans

- Auto loans

- Personal bank loans/ lines of credit

- Balances owned personally to friends or family

These will most likely be considered Long Term Liabilities- meaning it’s going to take over a year to pay them off.

You’ll also want to include short-term liabilities (those that will take less than a year to pay off):

- Credit card balances

- Taxes owed

Step 3: What's the difference?

Step 1- Step 2...Pretty simple- you got this!

Want this to be even more simple? Grab my personal net worth statement for free HERE! You can fill it out, save, and update to track your financial goals.

Step 4: Know your credit score and factor that in!

Your credit score is one of the most overlooked portions of your personal net worth. You credit score is a powerful tool that unlocks opportunities to leverage other people’s funds.

Better credit leads to savings on insurance, utilities, credit card fees, mortgage rates, closing costs and more!

Better credit can also unlock the lowest interest rates available, which allows more money to go into other income producing assets!

- Most banks allow you to access your FICO score- which is not one of your credit scores, but is a very good indicator of where you stand on your credit reports.

- Multiply the amount in Step 3 using the following scale:

Now there is your Adjusted Net Worth!

Step 5: Divide by your Adjusted Net Worth by your average monthly living expenses

This is a great exercise to give you an idea how many months you could live with ZERO income — exciting right?!

Are you surprised by this number?

Either way, hopefully this gives you an idea of where you are on your path to financial freedom, or the ability to live comfortably without working. And although there are many other factors that play into this and your liquidity — like having multiple passive income streams, appreciation from the stock market, physical assets, or the impact of inflation — this is a very basic way to do a spot check and watch your progress!

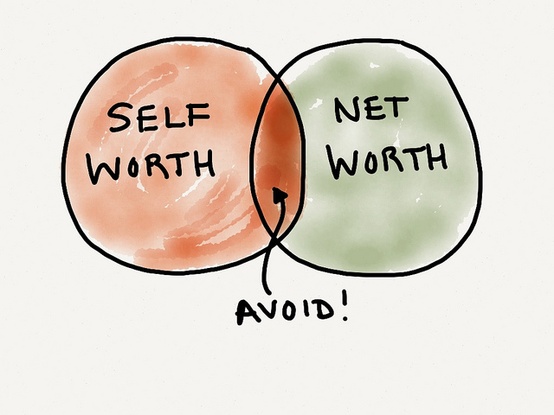

Step 6: Remind yourself that your Net Worth does not equal Your Worth

Image from George Schofield

When we start to really take a look at our personal finances, it can be easy to get overwhelmed by the numbers and what we feel we should be doing or have to be doing.

Personal finance is…. personal. Everyone’s dreams, goals, and finances look different and that’s OK.

Your net worth doesn’t define you- especially because it’s always changing- it’s just a snapshot in time, that’s it!

Remember that good people can have a negative net worth and bad people can have a positive net worth….so your number does not measure your goodwill, your awesomeness or how much people love you.

Step 7: Repeat!

Keep following this process on a regular schedule (utilize those reminder Apps in your phone!) to keep you focused on your goals, celebrate the wins, and track your progress on your journey to financial wellness!