9 Smart Tax Moves Every Woman in Her 40s Should Know in2026

Mar 01, 2026

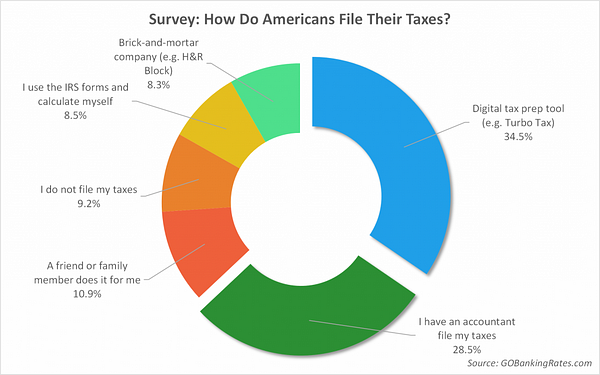

Doing My Own Taxes (And Knowing When It Was Time to Stop)

For 15 years, I did my own taxes. I even did taxes for friends and family. Doing taxes calls on my strengths of organization & attention to detail. Spreadsheets. Receipts. Late-night organizing sessions. No audits. No scary letters. 🎉

But in 2020, I started 2 businesses... Holistic Personal Finance and a LLC to manage our first rental property. The increase in complexity reminded me of somethingI learned early in my career working with wealthy clients:

Financial confidence isn’t about doing everything yourself. It’s about knowing when to bring in expertise.

If you’re in your 40s, there’s a good chance your tax situation is more layered than it was in your 20s or 30s. Let’s talk about it.

Should you file your own taxes?

If your tax situation is fairly simple, I encourage you to give it a go!

Simple can look like having:

-

W-2 income

-

Limited deductions

-

No business income

-

No major life changes (sale of property, stock windfalls, etc.)

But if you have some of the following:

-

Self-employment income

-

Rental property

-

Investment sales

-

Major life transitions (marriage, divorce, inheritance)

-

Significant deductions

Your situation starts to become complex and it may be worth building a relationship with a CPA, or using an upgraded version of your tax preparation software.

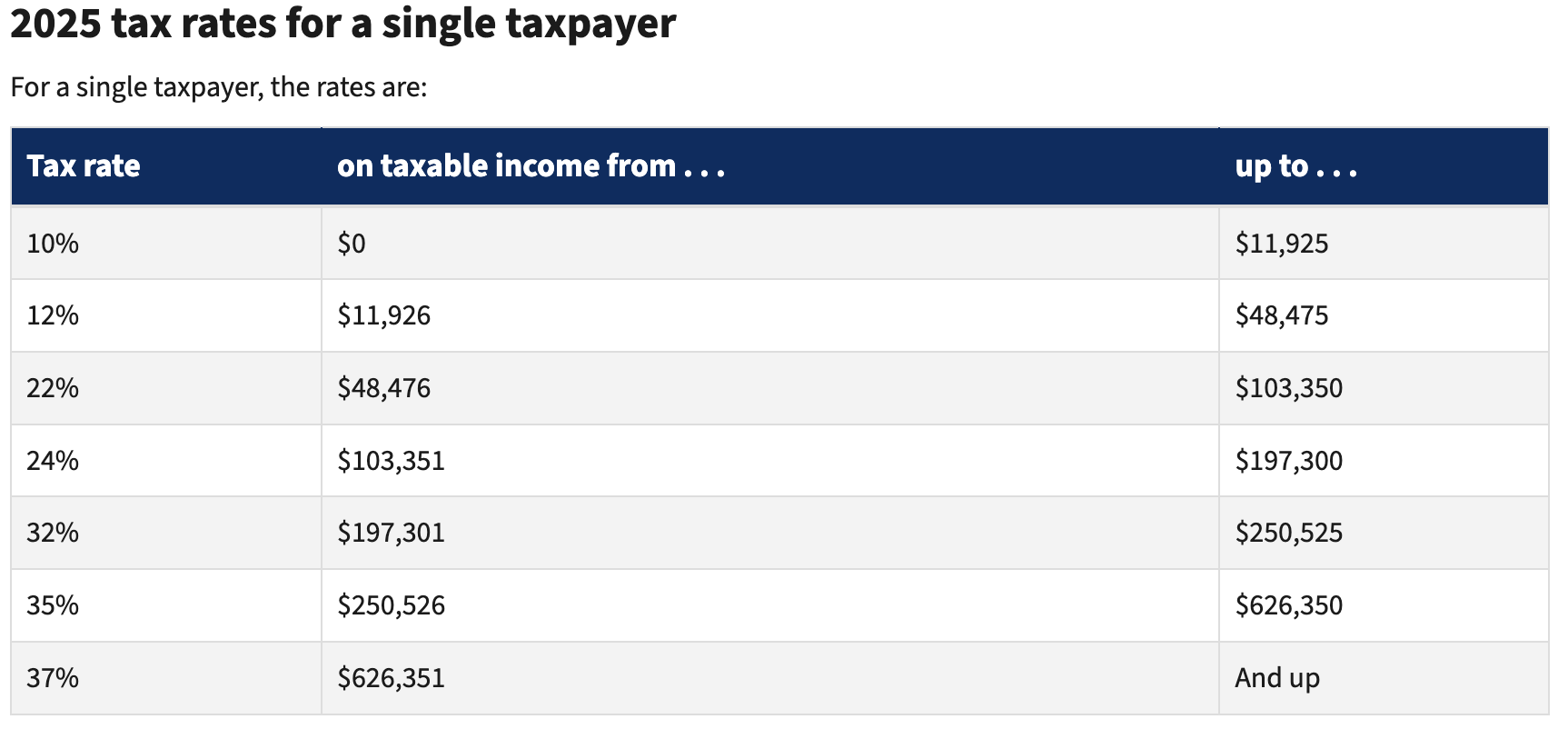

Quick Refresher: How Federal Taxes Work

We’re going to focus on Federal taxes here, since State taxes vary greatly. The Federal tax system is progressive. That means your income is taxed in layers (or “brackets”), not all at one rate. If you earn more, only the portion in the higher bracket is taxed at the higher rate, not your entire income.

You can think of your income being taxed in different buckets or brackets. It’s important to have an idea of where your taxable income lies in the bracket system. The single brackets are below, you can find the full list from the IRS --> HERE.

For example, if you are single and your taxable income is $110,000 you might be more motivated to try and use deductions or contributions to your 401k or Trad IRA to lower your taxable income to under $103,350 to save $1596 on your taxes owed (110,000-$103,350 = $6650. $6650*24%).

Most people don’t take into account that their taxes are a (somewhat) negotiable BILL. Yes, just like your housing payment. Not only that, but your taxes may be your biggest bill. So, take control today by learning more about how you can (legally) lower your tax bill. Understanding where your taxable income falls can also help you make smart decisions about:

-

Retirement contributions

-

Business deductions

-

Timing of income

-

Tax-loss harvesting

-

Charitable giving

9 Smart Tax Updates & Reminders for This Year

(Always confirm current IRS thresholds before filing — numbers adjust annually for inflation.)

1. The Filing Deadline Is Still April 15

If you need more time, file an extension, it gives you until October 15 to file. But remember: An extension to file is not an extension to pay. Penalties can reach 25% of unpaid taxes, so estimate and pay what you owe.

2. Standard Deduction Continues to Rise

The standard deduction increases most years due to inflation adjustments. For 2025 returns (filed in 2026), it’s higher than it was even a few years ago. For many households, itemizing no longer makes sense, but it’s worth running both scenarios if you’re close.

3. Max Out Retirement Contributions (Especially if You’re 50+ Soon)

Contribution limits increase over time and once you hit 50, catch-up contributions kick in.

This is a powerful way to:

-

Lower taxable income

-

Accelerate wealth building

-

Close retirement gaps

Your 40s are not the time to coast on retirement savings.

4. Don’t Ignore HSAs (If Eligible)

If you have a high-deductible health plan, your HSA is triple tax-advantaged:

-

Contributions reduce taxable income

-

Growth is tax-free

-

Withdrawals for medical expenses are tax-free

In a decade where medical expenses often increase, your HSA is a powerful tool for retirement (or early retirement) planning!

5. Review Your Withholdings

Many of my clients had to do this in 2025 and it's an important step in managing your tax bill. If you:

-

Got a raise

-

Changed jobs

-

Started a business

-

Got married or divorced

-

Added dependents

Your W-4 may need updating. HERE is an easy to follow guide to update yours (reminder you can do this ANYTIME!)

6. Be Strategic About Investment Accounts

If you’re investing outside retirement accounts, like a taxable brokerage account:

-

Understand capital gains taxes: Short term capital gains tax is the pricy one and that kicks in for assets sold within a year of acquisition. Long- term capital gains max out at 20% (although most people fall within the 0%-15% rate).

-

Be aware of dividend income: As you come closer to retirement, you will want to increase your dividend income, but doing so within your tax advantaged accounts (401k, 503b, IRAs, etc) might be a better place to do it than your taxable brokerage accounts to save you from paying taxes on dividend income.

-

Consider tax-loss harvesting: If you're investing in single stocks, I highly recommend doing so in a taxable brokerage account. This way, if you pick wrong or one stock goes sideways, you can harvest those losses against any gains you made and lower the amount owed.

7. Use the Child Tax Credit (If Eligible) & other benefits

Income phaseouts apply, but if you qualify, the federal Child Tax Credit (CTC) is worth up to $2,200 per qualifying child under age 17. Up to $1,700 of it is refundable, meaning you can receive this amount even if you owe no taxes. As kids get older, tax strategy shifts, especially approaching college years. If you have children you may want to look at the American Opportunity Tax Credit (AOTC) or Lifetime Learning Credit along with your contributions for 529 plans. 529 plans have had a major revamp in the past few years. You can read up on them HERE.

Also, if you had a child in 2025, make sure you register for the Trump Savings Account.

8. Know the 7.5% Medical Expense Rule

Previously the medical deduction threshold was 10% of AGI, but now (if you itemize) medical expenses exceeding 7.5% of AGI may be deductible. This matters in a decade where fertility treatment, major procedures and ongoing healthcare costs are more common.

9. Taxes Are Feedback — Use Them

The most financially confident women I work with don’t just “file and forget.” They:

-

Review their return

-

Adjust retirement savings

-

Reassess deductions

-

Plan for next year

Taxes show you how your money is flowing. That’s valuable feedback and data you (and your CPA) can use for next year!

Why Taxes Matter More in Your 40s

In this season of life, you may be:

-

In peak earning years

-

Earning bonuses or equity

-

Investing outside retirement accounts

-

Supporting children (or paying for college soon)

-

Caring for aging parents

-

Going through divorce or remarriage

-

Running a business or side hustle

-

Buying or selling property

Each of those comes with tax implications.

Final Thoughts

Taxes may be one of the least exciting areas of personal finance. Trust me, it’s much more fund to talk about investments, compound interest, or ways to save or make lots of money! So, if you’ve made it to the end of this blog- I commend you. I know this is a boatload of information, but the goal isn't to obsess over every detail. The goal is to be organized (yes, that means ALL YEAR), be informed of changes and know when to ask for help.

Overall, there are some great opportunities here- but you can’t take advantage of them if you don’t know about them. So, I hope you feel encouraged to do your research and lower that tax bill!